Many physicians put in up to 35,000 hours in training prior to going out into practice. I have found they receive about one or two hours of training or sound counseling on how to handle their personal finances when they make the jump to their higher salaries following their residencies or fellowships. They oftentimes spend more time planning their next vacation than the next 30-plus years of their own financial security.

To kick off this on-going series, this month I’ll propose a framework to build knowledge around. Keep in mind that page after page can be written on each one of the issues in this overview, but it is important to have a sense of the 30,000-foot view before diving into the specifics.

Building a Base

A sound financial strategy is not something that is quickly thrown together and then dusted off again once you approach retirement. It is something that you need to put significant thought into and monitor throughout your career and into retirement.

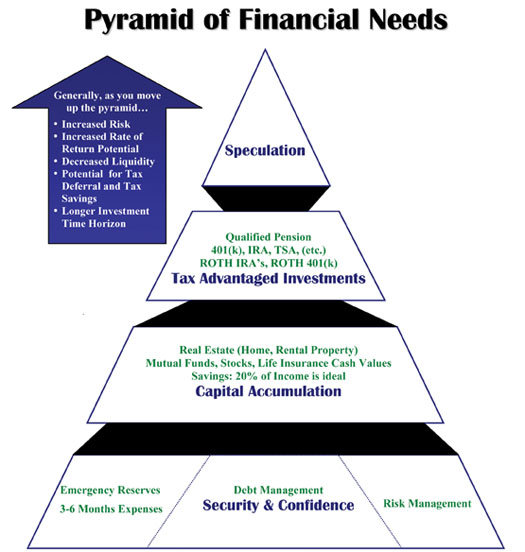

When working on assembling a financial strategy, you must spread your time and resources over many areas at once, all while prioritizing and attacking the areas of the highest need. The pyramid at left shows a starting point to visualize the main areas of need. Of course, the products and strategies will evolve, but each of these areas can be applied at all stages of a physician’s career.

The Security & Confidence Stage

Three areas should be made the priority of a financial strategy before moving to any advanced and more complex wealth-accumulation strategies. These make up the area that we would parallel to the “preventive care” of a physician’s financial strategy to avoid or guard against any financial issues in the future. Each of these three areas is no more or less important than the other two, and all should be given equal attention.

• Emergency Reserves. Emergency reserves should be in an account that emphasizes liquidity, safety and preservation of capital; the goal here is not rate of return. Unfortunately in today’s interest-rate environment, the best option is typically a money market account. The important item with reserves is to set a threshold of where you want this account to be and then not let your reserves continue to build up because it “feels good” to see a big number.

|

• Debt Management. The key to this second area of a financial strategy is the word “management,” not immediate debt elimination. Although it would be nice (and often very tempting) to never owe anybody anything, it is often not a shrewd long-term decision to eliminate long-term, low-interest debts sooner than necessary. A general rule of thumb is to eliminate debts aggressively at 7.5 percent or higher and to consider opportunity costs of the use of the money when the interest rate is lower.The idea is that if you put the same money into an investment vehicle that can potentially outgain the interest rate or cost of borrowing, you will increase your overall net worth throughout time. If you run the math on a difference of just out-investing your borrowing rate of 1 percent-plus over a long-term time horizon, the numbers eventually get very overwhelming and should help outweigh any urges that arise to pay off the mortgage or student loans earlier than scheduled.

It would be advisable to discuss this with a financial professional who can help quantify these decisions.

• Risk Management. The third area of financial strategy includes both consulting with an attorney on the legal documents that should be in place (e.g., wills, trusts, etc.) and obtaining the proper types of insurance. When you’re a med student, simple health, renter’s and auto insurance is typically what is needed; in residency and fellowship years, this expands to adding in specialty-specific disability insurance, umbrella liability insurance and, potentially, life insurance. When in practice, all of these types of coverage should be increased, and there should be an increased level of awareness on asset-protection concepts and which aspects of your net worth are protected from potential creditors. When progressing towards the end of a career, it would be prudent to analyze the need for long-term care insurance and life insurance for estate-planning purposes to protect the nest egg you have worked diligently to build.

|

Look for more detailed discussion of financial planning concepts in upcoming columns. REVIEW

Mr. Ylinen is a financial advisor with North Star Resource Group. He co-authored the book Real Life Financial Planning for Physicians. He maintains a national comprehensive financial planning practice that caters almost exclusively to physicians. The informatiom provided in this article is general in nature and are not intended to be specific recommendations. Please consult a financial professional for specific advice in relation to your individual circumstances.

For information on this topic or any other financial matter, direct your inquiries to his website,

askjonylinen.com.